Xiaomi’s growth model is already showing cracks

After crowing about how strong it is in India, and how loyal

its MiFans are, Xiaomi Corp can’t hold on to top spot in the

smartphone maker’s second-largest market.

Old nemesis Samsung Electronics Co pipped it in the June

quarter after ceding the lead to the Chinese company two

quarters prior, according to data released Tuesday night by

Counterpoint Research.

What should worry Xiaomi, and its investors, is that

fellow Chinese brands OnePlus and Honor both posted stronger

growth during the period.

Now that Xiaomi is a listed company, these numbers are more

than just an academic exercise.

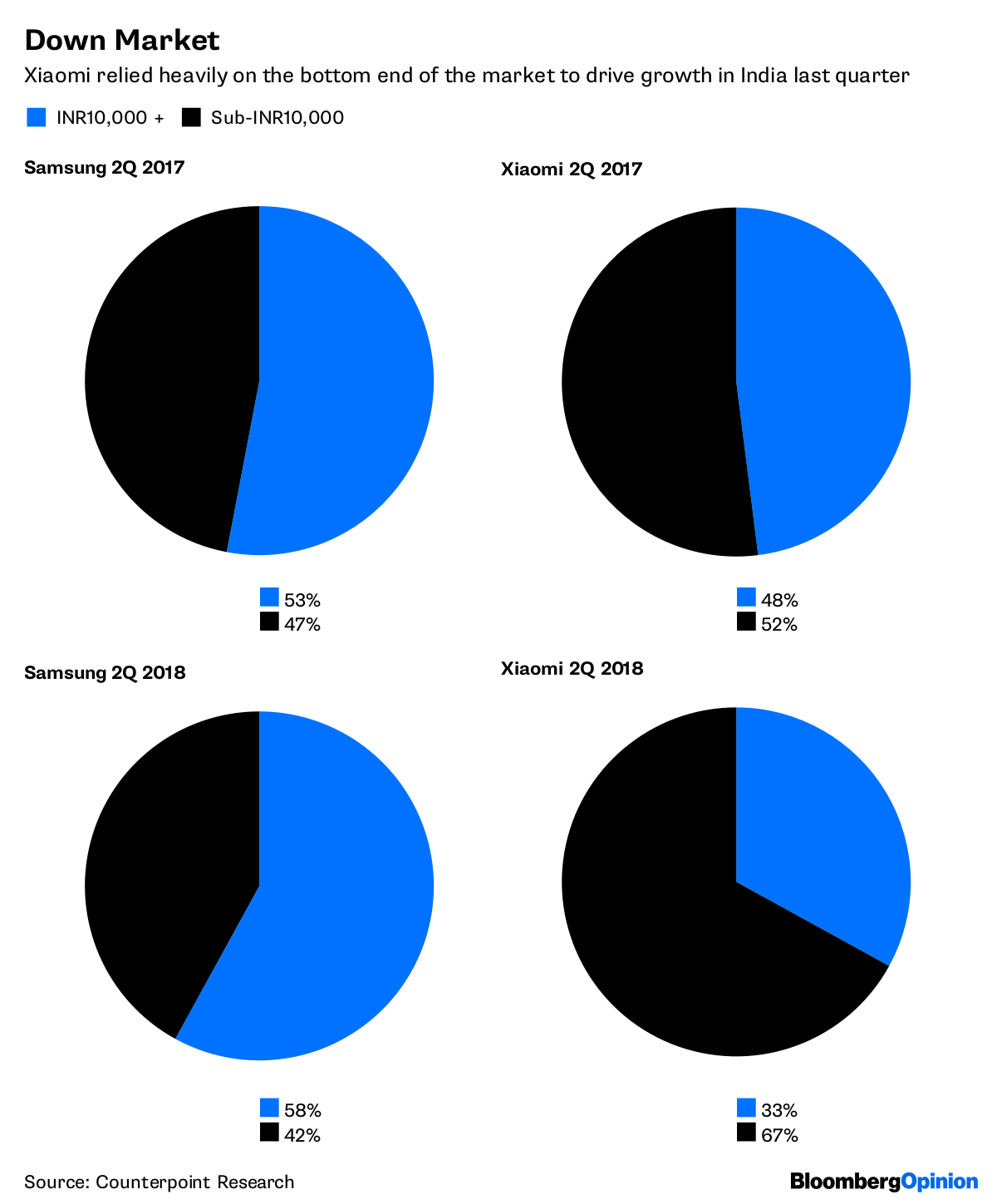

Dig further into the data and you’ll discover something

of greater concern. Xiaomi’s growth was even

more dependent on cut-price phones than in the past. Over

two-thirds of shipments were in the sub-10,000-rupee ($150)

category.

By comparison, Samsung took first place despite just 42% of the

devices it sold being in that price range. In other words,

there are plenty of consumers willing to pay for more

expensive devices.

Xiaomi likes to pretend that hardware profits don’t matter. And

we shouldn’t forget the red herring that founder Lei Jun threw

out back in May, when he made a song and dance about limiting

net-income margins on devices to 5%.

If we’re to believe that, then we need to buy into the view

that Xiaomi’s future is in the platform business, where it can

sell ads and other services. Underpinning this strategy is

getting Xiaomi devices into as many users’ hands as

possible, which is why selling smartphones on the cheap looks

like a reasonable trade-off for investors.

Yet cheap doesn’t buy loyalty. Samsung is proof of this. After

all, who’s the more loyal customer: Someone who

pays $150 for a smartphone, or someone who pays more than $500?

Apple Inc knows the answer.

That OnePlus shipments climbed 284%, according to

Counterpoint, and Honor posted a 188% increase,

highlights just how little loyalty Xiaomi has bought with its

low-price strategy – notwithstanding that its own 112

percent year-on-year growth is impressive.

If Xiaomi can’t provide investors with reasonable hardware

margins, and doesn’t garner much loyalty among MiFans upon

which to build its internet business, then investors need to

ask what the company really does offer.

No comments